Personal Finance 101: A Beginner’s Guide to Taking Control of Your Money

Simple, practical, and judgment‑free — because everyone starts somewhere

Why Personal Finance Feels So Hard (and Why It Doesn’t Have to Be)

If money stresses you out, you’re not broken — you’re normal. Personal finance comes with a lot of emotional baggage: stress, shame, avoidance, and the quiet belief that “everyone else seems to have this figured out but me.” Add in confusing jargon, contradictory advice, and social media highlight reels, and it’s no wonder many people avoid their finances altogether.

Let’s clear something up right away:

- You do not need to be good at math

- You do not need a high income

- You do not need to fix everything at once

Personal finance is less about intelligence and more about behavior, clarity, and consistency. This guide is designed to give you all three — without judgment, guilt, or overwhelm.

What Is Personal Finance, Really?

At its core, personal finance is all about managing your money. It encompasses everything from budgeting to saving, investing, and preparing for those unexpected rainy days. Think of it as the art of making your money work for you instead of the other way around.

This can be broken down into 5 core areas:

- Earn money

- Spend money

- Save money

- Invest money

- Protect money

That’s it.

It’s the system you use to make sure your money supports your life — instead of constantly stressing you out. When those pieces work together, money becomes a tool, not a source of anxiety.

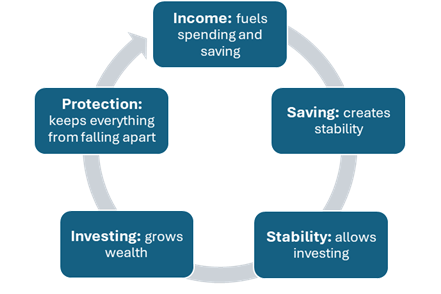

The Personal Finance Flywheel

Think of personal finance like a flywheel: The various components of personal finance are interconnected, forming a flywheel that propels individuals toward financial success. Each element, from earning income to protecting assets, influences the others, creating a dynamic relationship.

Skip the basics, and the entire system wobbles. Neglecting the foundational aspects of personal finance can lead to significant issues down the road. Without a solid understanding of these basics, individuals may struggle with managing their finances effectively, leading to long-term financial instability.

Before you plan the future, you need a snapshot of the present — no panic required. The first step is to understand your money in it’s current state.

Know Your Income

Start with what actually hits your bank account. It is essential to differentiate between gross pay, the total amount earned before deductions, and net pay, the amount received after taxes and other deductions.

- Gross pay: what you earn before taxes

- Net pay: what you actually receive

If your income varies, use a conservative monthly average; I recommend at least 6 months. Side income counts too — freelancing, overtime, reselling, anything. Exploring additional sources of income, such as part-time jobs or freelance work, can enhance financial stability. Understanding how to leverage these opportunities can provide an extra cushion and contribute to achieving financial goals.

Track Your Expenses (Without Guilt)

Knowing your expenses is a critical step towards your financial goals. Understanding the difference between fixed expenses, which remain constant each month, and variable expenses, which can change, is vital for effective budgeting. Once you have an understanding of your fixed and variable expenses split them into simple buckets and identify needs and wants.

- Fixed: rent, insurance, subscriptions

- Variable: groceries, gas, dining

- Needs vs wants (no shame — awareness beats restriction)

You don’t need perfection. A basic spreadsheet, banking app, or notes app works just fine.

Calculate Your Net Worth (Yes, Even If It’s Negative)

Net worth is a financial measurement that represents the difference between total assets and total liabilities. Understanding this concept is crucial for assessing overall financial health. To calculate net worth accurately, individuals must evaluate their assets, such as savings and investments, against their liabilities, which include debts like loans and credit card balances.

Net worth = assets – liabilities.

If yours is negative, congratulations — you’re normal. Student loans and early‑career debt make this extremely common. The goal is progress, not comparison.

Action step: Create your first money snapshot today. That’s a win.

Budgeting: Telling Your Money Where to Go

A budget isn’t about restriction. It’s about intention. A budget should be viewed as a tool for intention rather than a restriction on spending. It serves as a guideline to direct financial resources toward achieving personal goals and priorities.

Budgets fail when they’re unrealistic, overly strict, or built for someone else’s life. There is no such thing as a perfect budget — only a flexible one you actually use. Embracing flexibility in budgeting allows individuals to adapt to life’s uncertainties while still maintaining financial control.

Beginner‑Friendly Budgeting Methods

- 50/30/20 rule: This popular budgeting method suggests allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. It provides a simple framework for managing finances effectively.

- Zero‑based budgeting: This method requires you to assign every dollar of income a specific purpose, ensuring that all income is accounted for. It promotes financial discipline and encourages mindful spending.

- Pay yourself first: This strategy emphasizes the importance of prioritizing savings by setting aside funds before addressing other expenses. It encourages a proactive approach to building financial security.

- Bare‑bones budget: survival mode when money is tight. This method focuses on identifying and allocating funds only to essential expenses, allowing individuals to streamline their finances during tight times. It promotes financial minimalism and prioritization of needs.

How to Build Your First Budget

Building a budget can be a straightforward process if approached methodically.

- Start with income

- Cover essentials

- Assign savings (even small)

- Adjust — don’t quit

Your first budget is a draft, not a final exam. Read more about how to create a budget you will actually stick to here.

Saving Money: Your Financial Safety Net

Saving isn’t about wealth — it’s about stability.

Why Saving Comes Before Investing

Emergencies don’t wait for market returns. Without savings, every surprise becomes debt. Prioritizing savings lays a crucial foundation for achieving financial stability before pursuing investment opportunities. Stability provides a safety net that allows for growth without undue risk.

Emergency Funds Explained

An emergency fund is a dedicated savings account meant to cover unexpected expenses, providing peace of mind and financial security during challenging times. This fund serves as a financial safety net.

Determining the right amount for an emergency fund is essential, with recommendations typically suggesting saving three to six months’ worth of expenses, a starter fund can begin with a smaller amount to build momentum. The key here is to begin now and set aside money regularly.

- Starter fund: $500–$1,000

- Full fund: 3–6 months of expenses

- Where to keep it: high‑yield savings

Saving When Money Is Tight

It’s never too early to begin saving. Even small amounts can lead to substantial savings over time.

Keys to starting out when money is tight:

- Automate transfers to ensure money is being saved without the need to act.

- Start with $10 — momentum matters just as much as the amount.

- Use “invisible” saving strategies like rounding up purchases to save the difference.

Small, consistent actions compound faster than you think. We will expand on strategies to save money in future articles.

Sign up here for our email newsletter to be one of the first to know when.

Debt: How to Handle It Without Shame

Debt is a tool — sometimes useful, sometimes dangerous. Not all debt is created equal; some debts can be considered beneficial if they lead to asset accumulation, while others may be detrimental. Understanding the nuances of debt can aid in making informed financial decisions.

Common Types of Debt

- Credit cards an essential tool that can be both beneficial and detrimental; often carry high-interest rates and can lead to financial strain if not managed properly.

- Student loans these loans are often necessary for funding education, but they require careful management to avoid becoming overwhelmed with debt.

- Auto loans it’s common to finance your vehicle, however it is essential to understand the terms and interest rates to avoid taking on more debt than you can handle.

- Mortgages often considered beneficial for a number of reasons, these loans include long-term obligations and can be complex.

Not all debt is evil, but high‑interest debt is urgent.

How Interest Really Works

Understanding the difference between simple interest and compound interest is essential for grasping how debt can grow over time. Simple interest is calculated using only the original principle while compound interest adds in the accumulated interest along with the principal. Compound interest creates a “snowball effect” and can significantly increase the total amount owed if not managed carefully. Knowing how interest is being applied to your debt accounts is crucial to managing your debt smartly.

Compound interest works for you when investing — and against you when carrying balances.

Paying Down Debt

When debt is becoming out of control, selecting the best debt reduction strategy can make a significant difference in success. Often the major difference in strategies which work verse those that do not is related to your psychological preferences.

Two common debt reduction strategies are:

- Snowball method: focusing on paying off the smallest debts first, which can create a sense of accomplishment and motivate individuals to continue.

- Avalanche method: prioritizes paying off debts with the highest interest rates first, which can save money in the long run. This method requires discipline but can lead to substantial savings.

At the end of the day, the best method is the one you will stick with. We will be tackling this topic in more detail shortly.

Sign up for our newsletter to be one of the first to know when:

Credit Scores: The Adulting Score You Didn’t Ask For

A credit score is a numerical representation of an individual’s creditworthiness, affecting their ability to borrow money and secure favorable interest rates. Understanding its importance is essential for making informed financial decisions.

Your credit score affects:

- Loans

- Rent

- Insurance rates

What Impacts Your Score

- Payment history – one of the most significant factors. Make your payments on time!

- Credit utilization – how much of the credit you have are you using

- Account age – how long have you maintained your accounts

- Credit mix – variety in types of credit in use

- Inquiries – how often are you applying for new credit

The most important thing you can do to ensure a good credit score is to manage your personal spending habits and debt well. Pay your bills on time and make sure your budget is able to manage any new debt you choose to add.

Responsible use beats hacks every time.

Investing for Beginners (Without the Intimidation)

Understanding the difference between investing and gambling is crucial for recognizing the long-term benefits of financial growth. Investing involves making informed decisions with the expectation of generating positive returns, while gambling is primarily based on chance.

Investing isn’t gambling — it’s long‑term ownership.

When You’re Ready to Invest

Before taking on the challenges of investing there are a few pieces of your financial plan that should be in place:

- Emergency fund (3-6 months)

- High‑interest debt managed

- Long‑term mindset

Having said all of this, I firmly believe that anyone whom has a full-time job with a company that offers a retirement plan should initiate investing in this from day one. If your budget supports it, I would automatically invest enough to at least capture the maximum company match – this is extra money just asking to be given to you!

Beginner Investment Options

Beginning to invest early, even with modest amounts, can lead to substantial growth due to the compounding effect. That’s why I recommend starting as soon as you have a job which supports you through a retirement plan.

When first starting out index funds & ETFs are good options that provide a diversified portfolio with lower fees, making them ideal for beginner investors. They offer an accessible way to enter the market without extensive knowledge.

Before starting out, is it imperative to eductate yoursefl on how inversting works.

Protecting Your Money: Insurance Basics

Insurance is a crucial aspect of personal finance, serving as a risk management tool rather than a source of fear. It provides a safety net for unforeseen events, ensuring financial protection. Being without insurance can lead to significant financial burdens in the event of an emergency. Understanding the potential costs emphasizes the necessity of having adequate coverage.

Key types to know:

- Health

- Auto

- Renters/Homeowners

- Life (high‑level only)

Being uninsured is often more expensive than premiums.

Financial Goals: Turning Money Into a Life You Want

Setting financial goals across short, mid, and long-term timeframes is essential for achieving financial success. Examples include saving for a vacation (short-term), buying a home (mid-term), and retirement planning (long-term). Use SMART (Specific, Measurable, Achievable, Relevant, Time-bound) goals and tie money to values, not just numbers.

Consistency beats perfection — especially when life happens.

Common Beginner Mistakes (So You Can Avoid Them)

Mistakes are part of the process, not proof of failure. Below ar ebut a few mistakes people often make. The key is to stick with it and continue to learn and grow.

- Doing everything at once

- Copying someone else’s plan

- Ignoring automation

- Letting setbacks derail progress

Your 30‑Day Personal Finance Starter Plan

- Track spending, list debts, calculate net worth

Begin by monitoring where your money goes each month. This awareness is vital for understanding spending habits and making informed decisions. Create a comprehensive list of all debts, including amounts and interest rates. This overview will aid in prioritizing repayment strategies. Assess your financial health by calculating your net worth. This process involves evaluating assets and liabilities to understand your overall position.

- Build a basic budget, open savings account

Draft an initial budget that outlines your income and expenses. This foundational step is crucial for effective money management. Establish a dedicated savings account to start building your emergency fund. This step will enhance your financial security.

- Start emergency fund, automate one habit

Begin contributing to your emergency fund regularly. Even small contributions can add up over time, providing a safety net for unexpected expenses. Identify one financial habit to automate, such as savings transfers or bill payments. Automation streamlines financial management and enhances consistency.

- Learn investing basics, set 3 financial goals

Take time to research and understand the basics of investing. This knowledge will prepare you for future financial decisions. Identify three specific financial goals to work towards in the coming months. Clearly defined objectives will provide direction and motivation.

Frequently Asked Questions About Personal Finance for Beginners

Personal finance is how you earn, spend, save, invest, and protect your money so it supports the life you want — not just today, but long term.

Start by tracking income and expenses, creating a basic budget, and building a small emergency fund. You don’t need to invest or optimize everything right away.

There’s no perfect number. Even saving $10–$25 consistently builds the habit. Focus on consistency before increasing amounts.

Most beginners should do both: build a small emergency fund first, then focus on high-interest debt while continuing to save modestly.

All investing involves risk, but beginners can reduce it by focusing on long-term investing, diversified index funds, and simple strategies.

Final Thoughts: You’re Not Behind — You’re Just Starting

Personal finance isn’t a race.

Clarity creates confidence. Progress creates momentum. And you don’t need perfection to build a strong financial future — just a starting point.

You’ve already taken the hardest step: beginning.